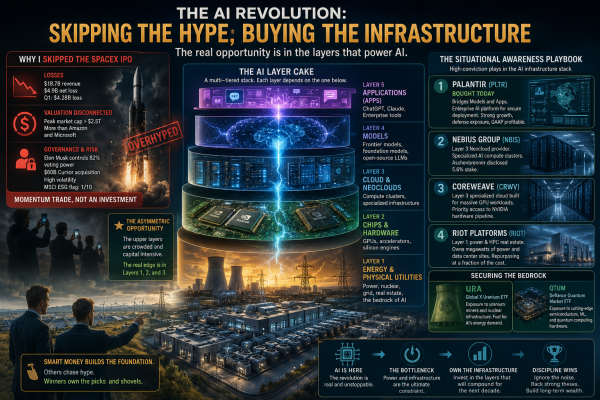

Why I Skipped the SpaceX HyPeO

Disclaimer: I am a random guy on LinkedIn, not your Financial Planner or Tax guy. What you read below are my opinions, not professional Stock recommendations.

If you are too busy to read the entire article, take a moment to absorb the visual summary below.

What Happened

The historic SpaceX IPO (SPCX) was the most anticipated public offering in history, making Elon Musk the world's first Trillionaire as the stock rocketed past $225 from its $135 IPO price. In the process it also created more than 4,400 millionaires among current and former employees. These millionaires include both corporate staff and blue-collar workers - such as machinists, welders, and cafeteria staff - because the company historically compensated employees at all levels with heavy stock equity in exchange for lower salaries.

Former SpaceX welder becomes a millionaire after historic IPO

Why I skipped SPCX

Well, I must come clean - I did try to buy the SPCX stock last Friday. At the opening price of $135. But no one was selling at that price. It opened effectively at $160, then went to $176. My limit order was cancelled. While SpaceX is undeniable as a vertically integrated monster spanning launch, Starlink satellite connectivity, and AI tools, the market has completely decoupled from fundamental reality, in part fueled by Podcast billionaires who are Elon Fanboys.

But Math doesn't lie. And here is the Math:

SpaceX reported $18.7 billion in revenue but posted a net loss of $4.9 billion, followed by another $4.28 billion loss in Q1 of this year alone.

At its peak last week, the market cap cleared $2.5 trillion - briefly making it more valuable than Amazon and Microsoft. Paying that kind of premium for a company bleeding billions, no matter how cool the rockets are, is a momentum trade, not an investment.

Governance & Risk

If you're looking at SPCX right now (June 23, 2026) thinking it's a "buy the dip" opportunity because it tumbled back to the mid-$150s today: be careful.Elon Musk controls over 82% of the voting power. Combined with an absolute avalanche of volatility following their $60 billion acquisition of the AI coding agent Cursor, and risks associated with Space exploration in general, the post-IPO honeymoon is officially over, lockup expirations and profit-taking are underway, and trading a story when the fundamental rubber has to meet the road is highly dangerous. It does not help that yesterday they launched a debut $20 billion, investment-grade senior unsecured bond offering to pay off outstanding bridge loans and fund its expanding artificial intelligence infrastructure.

- Launch & Constellation Backlash: Proposed AI compute satellites in sun-synchronous orbits have drawn heavy criticism from astronomers and regulators over light pollution. Additionally, ongoing lawsuits highlight environmental damage to delicate ecosystems and wildlife refuges near launch sites.

- Space Debris: The rapid scaling of the Starlink constellation increases orbital congestion and the risk of collisions, a major sustainability issue cited by rating agencies.

- Starship Development: While heavily touted for its massive payload capacity, the Starship program faces ongoing launch delays and technical challenges.

So which stocks did I buy this month?

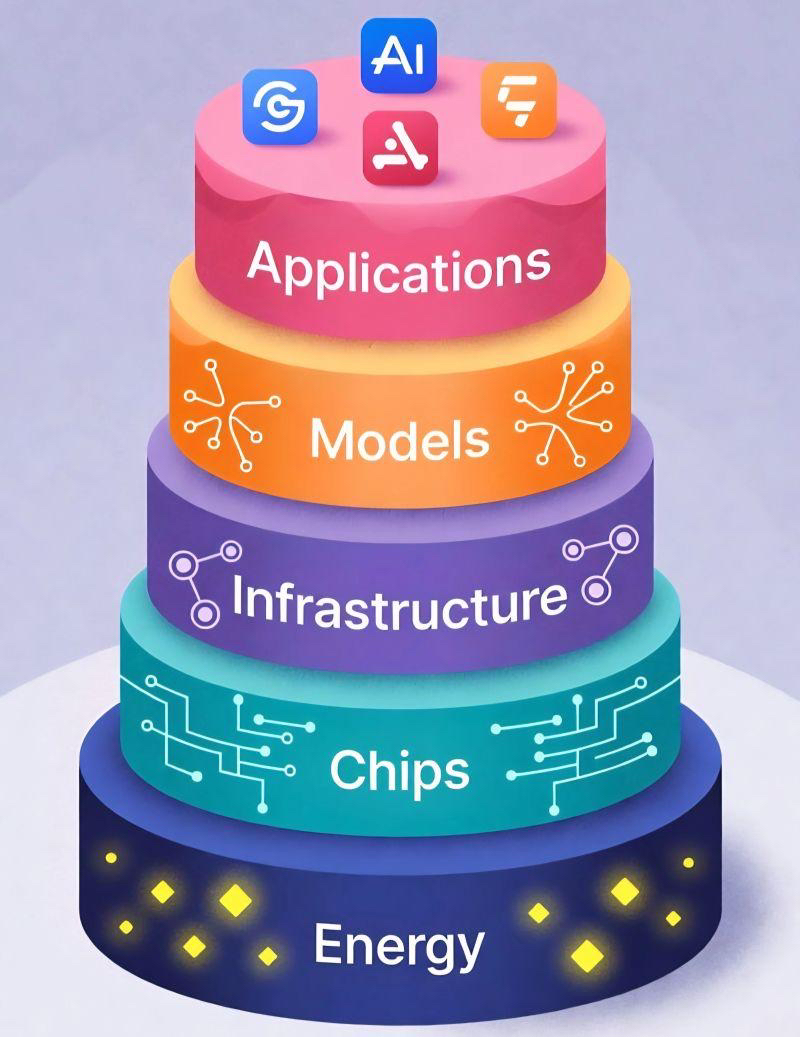

Instead of chasing rockets, I’m investing directly into what industry insiders call the AI Layer Cake.

The AI Layer Cake

To understand where to put your money, you have to look at the entire AI ecosystem as a multi-tiered stack. Each layer relies entirely on the one below it, but the risk and reward profiles are radically different:

Layer 5: Applications (Apps): This is the consumer/enterprise facing software layer (ChatGPT, Claude Code, hyper-specific enterprise tools). It’s fast-moving but hyper-commoditized with almost zero switching costs.

Layer 4: Models: The actual brains (OpenAI’s frontier models, Google’s Gemini, open-source Llama). This layer is locked in an incredibly expensive, capital-intensive arms race where today's king is tomorrow's legacy software.

Layer 3: Cloud & Specialized Infrastructure ("Neoclouds"): The compute nodes and specialized server architectures where these massive networks are actually built, trained, and hosted.

Layer 2: Chips & Hardware: The silicon engines powering it all - dominated by Nvidia’s advanced accelerators.

Layer 1: Energy & Physical Utilities: The absolute bedrock. AI requires an unfathomable amount of raw, gigawatt-scale electricity, nuclear baseloads, and data center grid connections.

Right now, the upper tiers (Models and Apps) are burning cash trying to out-compete one another. The real asymmetric opportunity is at the very bottom of the cake: Layers 1, 2, and 3.

The "Situational Awareness" Playbook

This structural view of the market is exactly what Leopold Aschenbrenner laid out in his definitive 165-page manifesto, Situational Awareness: The Decade Ahead. Aschenbrenner- a brilliant former researcher on OpenAI's Superalignment team—argues that the ultimate bottleneck to artificial general intelligence (AGI) isn't the software algorithms; it's the raw physical constraints of power grids and specialized data centers. Aschenbrenner isn't just writing essays; he is aggressively trading this thesis via his multi-billion-dollar fund, Situational Awareness LP. By tracking his high-conviction institutional positions and pairing them with my own thesis on the lower layers of the cake, I've aligned my capital with the literal backbone of the next decade.

Many of you know my core tech strategy: I’ve happily held the foundational tech giants -Google, Amazon, Meta, Microsoft, and Apple - for 15 years now, and I’m letting those multi-bagger positions ride. I also managed to secure a piece of Nvidia (NVDA) a year ago at $98, which has more than doubled to over $208 today. But to complement those structural tech anchors, here is the high-growth infrastructure playbook I've built out around Aschenbrenner's framework, including a major play today:

1. Palantir Technologies (PLTR) - Bought Today after months of skepticism about the P/E. I pulled the trigger on a major position in PLTR today. While others are building raw models, Palantir’s AIP (Artificial Intelligence Platform) bridges the gap between Layer 4 and Layer 5. It is the premier software layer enabling enterprises and governments to deploy AI securely, cleanly, and effectively. As a developer, I look at how enterprises struggle with context, data security, and LLM triage. Palantir solved this years ago. Their enterprise client growth is compounding, they are deeply entrenched with the U.S. defense sector, and unlike speculative AI plays, Palantir boasts clean GAAP profitability. Today's broader market pullback gave me the exact entry window I wanted.

2. Nebius Group (NBIS) Nebius is a core holding of the Situational Awareness fund, with Aschenbrenner recently disclosing a massive 5.6% stake in the company. Operating squarely in Layer 3 (Infrastructure), Nebius is a specialized "neocloud" provider that rents out full-stack, GPU-heavy clusters specifically optimized for massive AI training. Backed by elite-tier hardware commitments, they are building massive clusters to meet insatiable compute demand. Following Aschenbrenner into NBIS means owning a direct tollbooth on AI model training.

3. CoreWeave (CRWV) Sticking firmly to Layer 3, CoreWeave is another massive holding in the Situational Awareness portfolio (accounting for over 14% of his public stock exposure). CoreWeave is a specialized cloud provider built from the ground up for massive GPU workloads, securing priority access to Nvidia's hardware pipeline. While legacy cloud giants try to be everything to everyone, CoreWeave provides the lean, high-powered infrastructure that frontier labs rely on to train their largest networks.

4. Riot Platforms (RIOT) You might know Riot as a Bitcoin miner, but smart institutional capital views them as Layer 1: Power Infrastructure and High-Performance Computing (HPC) real estate. Aschenbrenner has built a massive position in Riot because crypto miners own the two scarcest resources of the AI era: megawatts of low-cost, grid-connected power and permitted data center real estate. Repurposing or dual-allocating these facilities for AI compute costs a fraction of building a data center from scratch.

5. Securing the Bedrock: URA & QTUM ETFs : To round out this thesis and capture the broader macro tailwinds of the lower layers, I’ve also taken positions in two highly strategic ETFs:

Global X Uranium ETF (URA): If you believe in Layer 1, you have to believe in nuclear energy. Hyperscale data centers require zero-carbon, 24/7 continuous baseload power, which solar and wind simply cannot provide on their own. URA gives me broad exposure to uranium miners and nuclear infrastructure components that will fuel AI's energy demand.

Defiance Quantum Market ETF (QTUM): This handles Layer 2. QTUM tracks companies at the absolute cutting edge of machine learning, advanced semiconductors, and quantum computing hardware. It’s an excellent, diversified way to own the physical compute engines without betting on a single chip manufacturer.

🫤 Dileep's Skeptical Takeaway:

SpaceX is an amazing company, and its IPO last week was a watershed moment both in terms of the sheer scale at $2T+ as well as the potential of the Technology itself. Having said that, Space is unforgiving, and in the short term I prefer to bet my $ on the Tech humans are deploying right here, on Earth.

Enjoying What the AI?

Get a new edition every week, plus join the conversation on LinkedIn.

Subscribe on LinkedIn